+

+Feature engineering, time series stationarity checks are few of the use-cases that are compiled in this gists. Check

+individual module defination and functionalities as follows.

+

+## Stationarity & Unit Roots

+

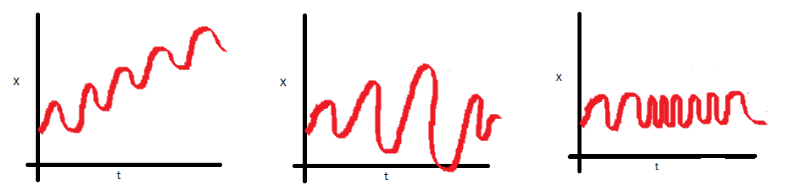

+Stationarity is one of the fundamental concepts in time series analysis. The

+**time series data model works on the principle that the [_data is stationary_](https://www.analyticsvidhya.com/blog/2021/04/how-to-check-stationarity-of-data-in-python/)

+and [_data has no unit roots_](https://www.analyticsvidhya.com/blog/2018/09/non-stationary-time-series-python/)**, this means:

+ * the data must have a constant mean (across all periods),

+ * the data should have a constant variance, and

+ * auto-covariance should not be dependent on time.

+

+Let's understand the concept using the following example, for more information check [this link](https://www.analyticsvidhya.com/blog/2018/09/non-stationary-time-series-python/).

+

+

+

+

+

+| ADF Test | KPSS Test | Series Type | Additional Steps |

+| :---: | :---: | :---: | --- |

+| ✅ | ✅ | _stationary_ | |

+| ❌ | ❌ | _non-stationary_ | |

+| ✅ | ❌ | _difference-stationary_ | Use differencing to make series stationary. |

+| ❌ | ✅ | _trend-stationary_ | Remove trend to make the series _strict stationary. |

+

+

+

+```{eval-rst}

+.. automodule:: pandaswizard.timeseries.stationarity

+ :members:

+ :undoc-members:

+ :show-inheritance:

+```

+

+## Time Series Featuring

+

+Time series analysis is a special segment of AI/ML application development where a feature is dependent on time. The code here

+is desgined to create a *sequence* of `x` and `y` data needed in a time series problem. The function is defined with two input

+parameters (I) **Lootback Period (T) `n_lookback`**, and (II) **Forecast Period (H) `n_forecast`** which can be visually

+presented below.

+

+

+

+

+

+

+

+```{eval-rst}

+.. automodule:: pandaswizard.timeseries.ts_featuring

+ :members:

+ :undoc-members:

+ :show-inheritance:

+```

+

+